How to build your value proposition

With change comes your chance to explore new perspectives.

To succeed in any business – and particularly as a financial adviser – you need to clearly, succinctly articulate the reasons clients should engage your services or invest in the products you recommend.

Your clients need to understand what you do, the benefits of your advice, the quality of the financial products and services you offer, and how these products and services align with their needs and preferences.

They need to know what sets you and your firm apart, and what value you can deliver to them. They need to appreciate the merit of having an ongoing relationship with you and your business.

Whether you operate your own AFS licence or are aligned with a large, multi-adviser dealer group, your clients ultimately have a business relationship with you, as an individual. They need to trust that you can help them solve financial problems and embrace financial opportunities.

Your combination of professional strengths and specialisations is unique to you and your business. Likewise, each client has a combination of needs, challenges and preferences that is unique to them.

The value you provide lies at the specific point at which your capabilities intersect with your clients’ needs.

Too many financial advisers try to be ‘all things to all people’. In any business, industry or profession, this is a recipe for failure. Too few advisers have a compelling value proposition that clearly explains what they do, who they serve, and how they provide value to the people they serve.

If you have yet to articulate your value as a financial adviser, please read on. This guide will help you build and communicate a compelling value proposition that will boost your marketing efforts and enhance the core efficiency and effectiveness of your financial advisory practice.

In essence, your value proposition is a business identity statement and a promise to your clients.

It is a concise statement that explains:

Your value proposition articulates why clients should initiate or maintain a professional business relationship with you. It is a positioning statement that explains how you and your services are a better choice for your ideal clients than any alternative. It explains how you can solve your ideal clients’ problems and help them make the most of opportunities.

Sue Viskovic, founder and managing director of Elixir Consulting (a business coaching agency for financial advisers), says a value proposition, at its core, is a clear explanation of what you do for your clients.

“I talk about value propositions in terms of two measures,” Viskovic says. “There is the marketing piece – the language you use, or the descriptive statement you use, to describe the value you offer to clients. This is used across all your marketing materials to help you attract clients and to help them see what you stand for, and why they might want to chat with you.

“Once the client is in front of you, and speaking with you, you need to tailor it in a personal way to the individual needs of that client.”

A value proposition statement should be simple. It should distil your larger sales or marketing messages into a clear explanation that your ideal client can easily understand, appreciate and remember.

Where value = benefits – costs, your value proposition explains why paying fees in exchange for your services is an astute decision for your ideal clients to make. If developed appropriately, it can serve as the foundation of your practice in many ways.

For example, it can:

Rob Jones, CEO and managing director of Peloton Partners (a consultancy that helps financial services companies to reach their potential), says the concept of value – as articulated in a value proposition – is critical for financial advisers, and should include a combination of the intangible and tangible factors of advice – how we make people feel, and what we do for them.

“The intangible factors involve the reasons clients sought an adviser in the first place,” says Jones. “For example, they may have needed someone to help them organise their financial affairs, giving them the peace of mind they crave.

“So, the number one factor is intangible value. Then, of course, tangible value is simply the physical things we must do for clients, to convert the plan into reality.

You can develop your value proposition by following a series of four relatively simple steps:

While simple, this process is not necessarily easy. It may take considerable time and effort, but it will certainly pay off for you and your business over the long term.

Step 1 is to understand your target audience – the people you want to read and understand your value proposition.

Who are your existing clients? Who are your ideal (prospective) clients? What specific needs and problems do your clients and prospective clients have? What things do your clients value most highly?

If you don’t already have clear answers to these questions, you should begin asking.

Undertake market research, by asking your clients directly and individually, arranging a focus group, or conducting a survey. Don’t forget to ask other stakeholders – such as your employees, colleagues and other advisers – for their perspectives.

Once you have a clear perception of who your clients are, you then need to understand their core financial needs and problems.

You can do this by asking your existing clients questions such as:

Your research into your existing and ideal clients may involve some depth, including factors such as age, gender, income, location, demographic profile, lifestyle preferences, relationship status and other family circumstances.

Sue Viskovic suggests identifying your ideal clients in terms of personas or avatars.

“You need to bring the personas to life and understand the problems they want to solve,” Sue says.

“For example:

Bob is a 45 year old IT manager who earns $200,000. Mary-Jane is a 42 year old who earns $80,000. They have 2 children and live in a house in Carnegie. The things that are important to them are family time, socialising with friends, gardening and the occasional holiday. Their challenges include finding enough time in their days, understanding concepts of investments and not being able to save.

“Then you ask: ‘If I was to talk with Bob and Mary-Jane, what would I want and expect to hear from them, if they were to articulate what I do for them that they value?’ Their answers might include tangible things like ‘Save money on tax’, but there are also likely to be intangible things like: ‘I know I can just send an email and my adviser will action it, without me having to go to their office.’”

Download your free customer journey map at www.netwealth.com.au/innovation

As suggested, your business represents a unique combination of professional strengths, specialisations, areas of expertise, services and products that you offer and deliver to provide ultimate long-term value to clients.

Before you begin to write your value proposition statement, you need to understand these elements in detail. For example, what areas of expertise do you currently specialise in? Specific investment strategies? Self-managed superannuation funds? Retirement strategies? Business succession planning? Or full-service financial advice?

In your long-term future, which areas do you wish to continue specialising in? Which areas do you enjoy most? Which are you best at? Which are the most profitable? Which give you the greatest satisfaction and fulfilment?

These are the areas you should focus on. In any profession, you are most likely to succeed in the specific types of work that you enjoy the most.

Sue Viskovic suggests a key step in building your value proposition is to identify all the things you currently deliver, or would like to deliver, to clients.

“This might include specialisations [that relate to the education and technical knowledge of your advisers],” Sue says. “It might be the ability to handle finance and debt management. It might be SMSFs. It might be your understanding of a range of estate planning laws that you can draw on to help clients with their succession planning.

“It’s one thing to say, ‘This is what I do, and this is why you should come to me’. You then have to make sure that you have an appropriate way of delivering your services to satisfy the promise you are making.”

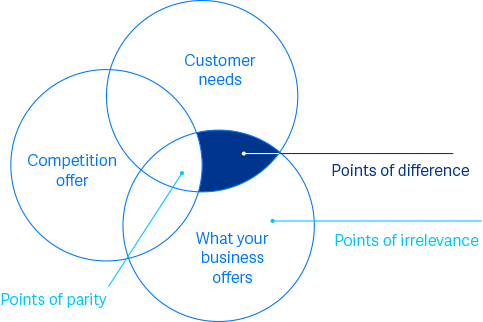

Knowing your business also involves identifying your competitors and your points of competitive difference in the advice market.

To distinguish your business, you should know who your competitors are, what they promise, what they deliver, what they stand for, and the ways in which they are similar or different to you.

The value you deliver to clients lies in the place where your areas of expertise intersect with your clients’ needs and problems.

To appreciate and articulate this intersection, you might ask:

It pays to make a list of the ways in which your business, your products and your services can help people, and the specific benefits they derive. Write down the ways in which your services and products solve real problems in ways that others don’t.

How will engaging with your business save your ideal clients money, time and effort? How will your business make money for your ideal clients? How can you ensure that your ideal clients consistently feel good about the experience of interacting with your business?

For each client need and problem that you have identified, can you identify a matching service or product that you already offer? For those problems that you cannot easily address, do you need to develop additional services or products? Or do you need to develop relationships with referral partners to address these specific client needs?

Once you can demonstrate that your business is directly relevant to your clients, you will be in a position to explain the value you offer and to create a compelling sales message that encourages clients to act.

After you have collected and collated sufficient information about your clients, your business and how the two intersect, it’s time to begin writing your core value proposition statement.

This is a statement that answers your target clients’ questions: ‘Why should I engage your business to provide financial advice to me?’ and ‘How do your financial services and products, and the fees you charge, represent genuine value to me?’

The format of your value proposition statement might include:

The following are examples of how advisers might apply these:

These are brief, general examples. Your value proposition statement, to be truly effective, is likely to be more detailed, specific and comprehensive. You can also create a series of value propositions, based on the detailed needs of different ideal client personas.

To begin expanding your value proposition – making it more authentic and inspirational for both you and your clients – you may wish to include a sentence or two that aligns with your business’s vision or mission statement.

For instance, if your business mission includes a commitment to specifically helping young people, or women, or if you specialise in promoting investments that support environmental sustainability, you would include this information in your core value proposition statement.

At the end of the day, your value proposition helps you to provide the services and products you believe in to clients you enjoy interacting with (and with whom you share similar values). It articulates what your business stands for and what sets it apart from others.

As mentioned in the previous chapter, if you have multiple targeted clients, you can also develop multiple value proposition statements – e.g. perhaps one for small business owners, one for retirees, and one for younger people.

Another way of expanding your value proposition is to follow the suggestions of Michael Kitces and Mitch Anthony, by considering value in terms of ‘return on life’ (ROL) rather than just ‘return on investment’ (ROI). In a 2015 blog post, Kitces wrote that Anthony had “put forth what may be the best set of terminology I’ve ever heard for articulating the true client-centric value proposition of financial planning.”

The terminology is contained in the following “six key value propositions of financial planning” that advisory businesses can use to articulate the ROL value they offer to clients:

As Kitces explains, “while the words themselves are not necessarily new and unique, Anthony’s use of them, along with explanations of exactly what the advisor provides, and how … paint a remarkably clear picture of what the intangible service of financial planning is meant to provide, and why it’s worthwhile for consumers to pay for a financial planner.”

Once you are satisfied that your value proposition is accurate and true to your business, your vision and your clients’ needs, it’s time to use it in as many different contexts and as many permutations as possible.

Don’t leave it to languish in a folder on your computer desktop. You need to bring it to life.

At the very least, versions of your core value proposition statement should be prominent on your website, in your marketing collateral and on your social media pages (Facebook, LinkedIn, Twitter, Instagram etc).

“There are different ways of bringing your value proposition to life these days,” says Sue Viskovic. “It doesn’t have to be static.”

“Nowadays, however, it might be more like pulling apart certain elements of the value proposition that clients will pay you for, and you might put together a video on each one of them.

“You might include the video on your Facebook page and then boost the post to specific target audiences that comprise the types of clients you are looking for.

“Or you might ask for testimonials from your clients that capture exactly what you do that they love and have them tell the story for you.”

Your value proposition should permeate every element of your business, including all business development or sales conversations.

When you meet with someone for the first time in a business setting, and they ask, “What do you do?”, you can deliver your core value proposition statement (as a kind of ‘elevator pitch’). Alternatively, you can initiate a more in-depth conversation by introducing one or two elements of your value proposition and following up with questions that enable you to customise the proposition to their individual circumstances.

For instance, you might begin simply by saying, “I help people to organise their financial affairs”. You can then ask the other person what they do, thereby identifying whether they are a prospective customer, a potential referrer, or any kind of relevant stakeholder in relation to your business.

Thereafter, the conversation can unfold naturally, with you asking more questions and articulating your value proposition in the context of their specific needs and preferences.

Once you have written your core value proposition statement – and have used it in your business for some time – it pays to review it regularly to ensure it continues to be inspirational and relevant for your business and for your clients.

To do this, ask yourself questions such as:

The answers to these questions will help you to constantly evolve your value proposition and remain relevant in the eyes of your clients.

Ultimately, however, any value proposition is worthless if you, and your people, don’t live up to it every day.

As a financial adviser, one of the worst offences you can commit is to promise one thing and deliver another – or fail to deliver at all.

For example, if your value proposition includes a promise to bring discipline to your clients’ financial affairs, it’s not enough to present an initial financial plan and leave the implementation of that plan entirely up to them. You need to collaborate with them, on a regular basis, to review each stage of implementation and provide hands-on support to ensure they achieve continuous improvement.

As investment advice is increasingly commoditised, your responsibility (and privilege) is to partner with your clients, advise them, and deliver undeniable (tangible and intangible) value to them over the long term.

How to build your value proposition

Learn how to clearly and succinctly articulate the reasons clients should engage your services or invest in the products you recommend.

Best interest duty & platform advice

Explore why you need to look beyond price to meet your client needs and legal obligations when it comes to platform selection.

Managed accounts during volatility & beyond

Learn from four wealth professionals how managed accounts can enhance your client value proposition during volatile times and beyond.

How to attract & retain high new worth clients

Explore seven strategies to evolve your service offering and attract more high net worth individuals as clients.

Your own AFSL - What you need to know

Understand the benefits, challenges and tips for businesses looking to self-licence, and how to apply for your own AFSL.

How to choose the right dealer group

Identify the key criteria for assessing which dealer group you should join, and why price should be the least important factor.